Many of us were told that house prices are so high because there are too many people and not enough houses. While this is true, house prices have also been pushed up by the hundreds of billions of pounds of new money that banks created in the years before the financial crisis.

1. Banks created hundreds of billions of pounds and put it into property

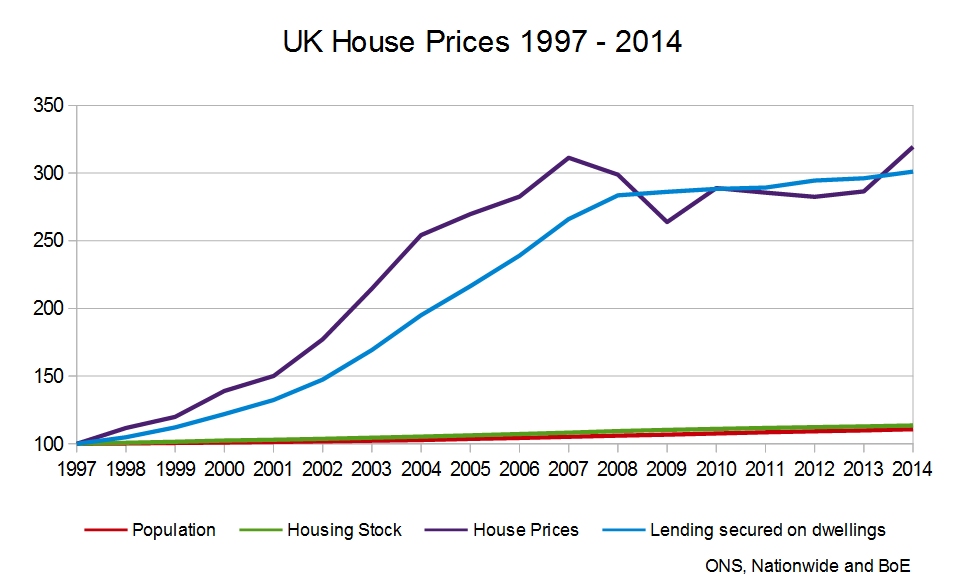

In the ten years up to the start of the financial crisis, house prices tripled. Many people think this is because there were not enough houses around, but that is only part of the picture. A major cause of the rise was that banks have the ability to create money every time they make a loan. During the period in question the amount of money banks created through mortgage lending more than quadrupled! This lending was a major driver of the massive increase in house prices.

2. House prices rise faster than wages

House prices rise much faster than wages, which means that houses become less and less affordable. Anyone who didn’t already own a house before the bubble started growing ends up giving up more and more of their salary simply to pay for a place to live. And it’s not just house buyers who are affected: pretty soon rents go up too, including in social housing.

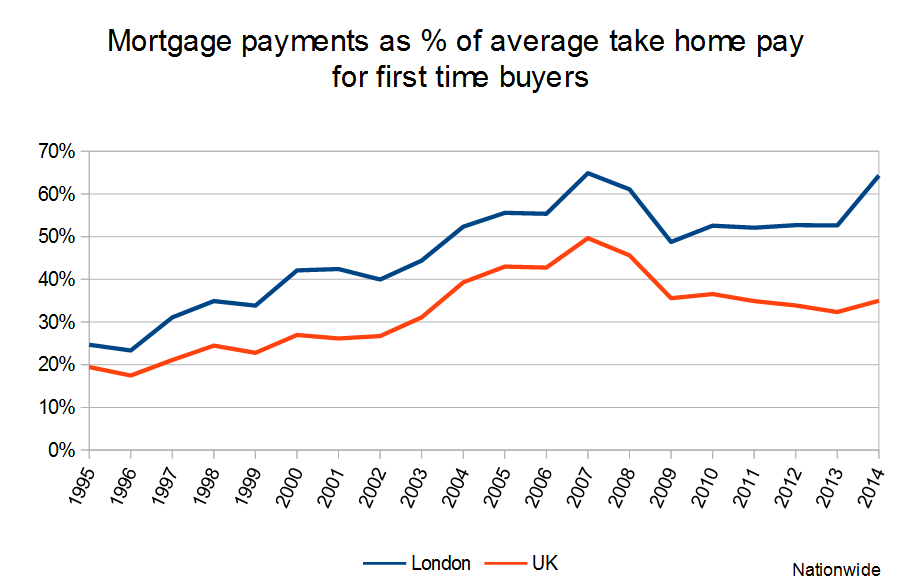

This increase in prices led to a massive increase in the amount of money that first time buyers spent on mortgage repayments. For example, while in 1996 the amount of take home salary that a first time buyer would spend on their mortgage was 17.5%, by 2008 this had risen to 49.3%. In London the figures are even more shocking, rising from 22.2% of take home pay spent on their mortgage in 1997 to 66.6% in 2008.1

3. House price bubbles benefit almost no-one

Asset price bubbles and the speculative behaviour associated with them tend to cause financial crises, which lead to lower growth, higher unemployment and higher government debt. High house prices also act as a mechanism for transferring wealth from the young to the old, from the poor to the rich, and from those that don’t own their own home to those that do. Even those with housing don’t benefit massively from higher house prices – after all, we all need somewhere to live, and anyone selling their home will find that on average other house prices will have risen by the same amount, leaving them no better off. In reality, only the banks and those with many properties benefit from high house prices: high prices mean that people will have to take out larger mortgages for longer periods of time, which means more money in interest payments for the banks.

1. Source: Bank of England Statistical Database and Nationwide House Price Survey