Because almost all of our money is ‘on loan’ from banks, someone has to pay interest on nearly every pound in the UK. This interest redistributes money from the bottom 90% of the population to the very top 10%. Meanwhile, inflated house prices and financial instability all lead to a growing gap between the poor and the rich.

1. The system distributes money from the bottom 90% to the top 10%

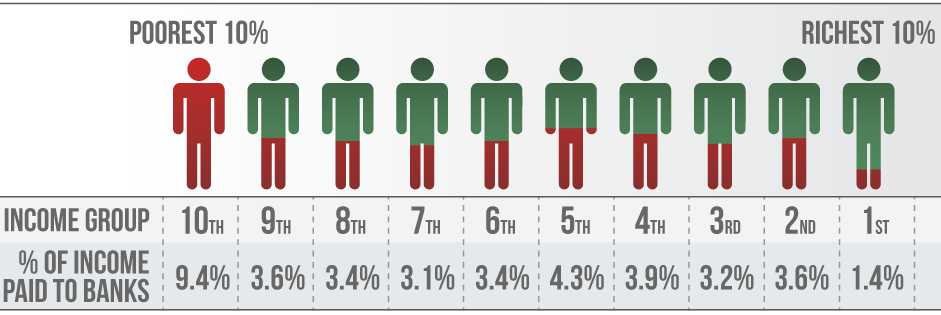

Because 97% of the money in the UK is created by banks, someone must pay interest on nearly every pound in the UK. The bottom 90% of the UK pays more interest to banks than they ever receive from them, which results in a redistribution of income from the bottom 90% of the population to the top 10%. Collectively we pay £165m every day in interest on personal loans alone (not including mortgages), and a total of £213bn a year in interest on all our debts.

Relative distribution of wealth drain from banking sector

2. It transfers money from the real economy to the banks

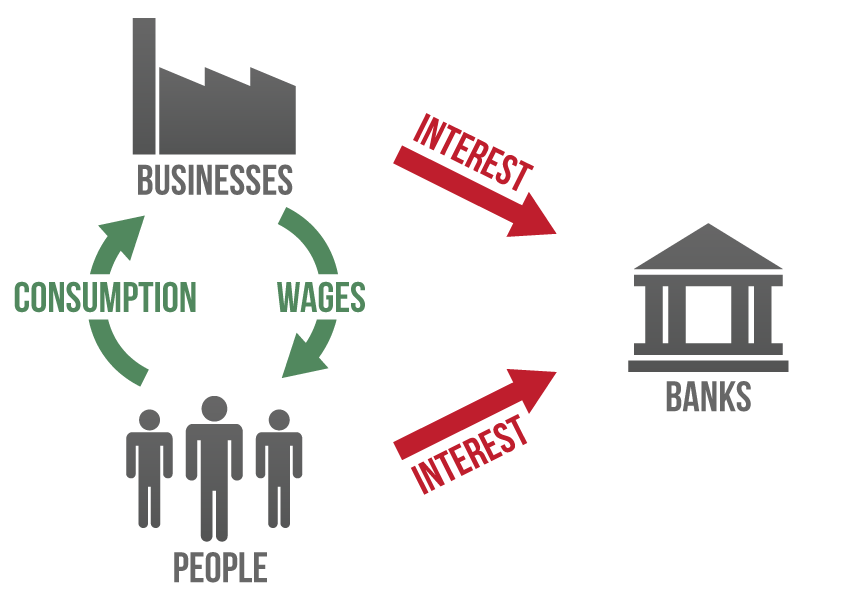

Businesses are also in a similar situation. The ‘real’ (non-financial), productive economy needs money to function, but because all money is created as debt, that sector also has to pay interest to the banks in order to function. This means that the real-economy businesses – shops, offices, factories etc – end up subsidising the banking sector. The more private debt in the economy, the more money is sucked out of the real economy and into the financial sector.

3. It transfers money from the rest of the UK to the City of London

Banks pay their staff out of their profits, which in large part comes from the interest they charge on loans. Because most of the high earning bank staff work in the City of London, this results in a geographic transfer of wealth from the UK to those working in the City of London.

4. The instability that the system causes means that temporary and low-paid jobs are insecure

When banks cause a financial crisis the subsequent recession leads to an increase in unemployment. It tends to be low-paid and temporary contract workers who are the first to get made redundant, so that instability in the economy has a bigger effect on those on low incomes with insecure jobs.

5. High house prices increase inequality

When house prices are pushed up by banks creating money, those on low incomes suffer the most – they won’t be able to get a mortgage big enough to buy a house, so they won’t benefit from the higher prices. Younger people also lose out, as the cost of buying their first house swallows an ever larger amount of their income. Meanwhile, those who can get access to mortgages can buy multiple houses and thus benefit from the inflation in asset prices. In large part these people tend to be older and wealthier. This all increases inequality across different income groups and between the young and old.

Evidence

The evidence compiled in this paper suggests that the current monetary system contributes to the growth of inequality through several channels.

Read “Banking, Finance and Income Inequality (Free, PDF, 16 pages)

If we want to tackle inequality, we need to change the way that money is created.