Are banks really the powerhouse of the UK economy? Or could they be some of the most heavily-subsidised businesses in the world?

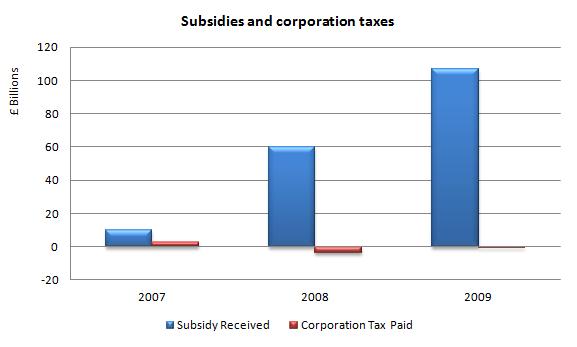

The chart below shows how much banks pay in taxes, and how much they receive in hidden subsidies. Shockingly, it seems that banks receive far more in subsidies than they ever pay in taxes.

- Source: Bank of England statistical database. Andrew Haldane, The $100 Billion Dollar Question (available at http://www.bankofengland.co.uk/publications/Documents/speeches/2010/speech433.pdf)

Update: the Bank of England has just released a new paper which looks at the different ways of estimating the subsidy the state provides to the banking sector. In short, the size of the subsidy is dependent on the methods used to estimate it. The chart below shows how much the estimates vary using different results, with the authors concluding that “despite their differences, all measures point to significant transfers of resources from the government to the banking system.”

- Source: Bank of England, Financial Stability Paper No. 15 – May 2012.

“The implicit subsidy of banks”. Joseph Noss and Rhiannon Sowerbutts

How do we subsidise banks?

Under the current banking system the money in your account is not really money at all, it is simply a debt which your bank owes you. Because banks actually hold very little in the way of real money (i.e. cash or central bank reserves) compared to their customer deposits, if everyone came and asked for their money back the bank would run out of money pretty quickly. Even the rumour that other people may be about to take their money out of a particular bank might start a ‘run’ on that bank. And once a run starts on one bank, customers of other banks start to panic, and try and withdraw their money out their banks.

To stop this happening, the government guarantees the money in your account, saying that if the bank goes bust, the government will reimburse you that money (up to £85,000). This scheme is called ‘deposit insurance’, or specifically, the Financial Services Compensation Scheme.

However, by giving people insurance you change their behaviour (known in economics as moral hazard). In a world with no deposit insurance if a bank went bust its customers would not receive any money in exchange for their deposits. This would lead them to monitor the banks behaviour and decisions much more closely, to ensure that the bank was not taking unnecessary risks which could jeopardise their deposits. Knowing that there was the possibility of losing all or some of the deposits would also lead the customers to demand a much higher rate of interest on their deposits to compensate them for the risk.

Because we have deposit insurance in the UK depositors do not monitor their banks behaviour, which means banks can behave in a riskier way than they otherwise would be able to. They can also pay a lower rate of interest to depositors, saving them money.

However, banks also borrow large amounts of money from other banks and institutions on the money markets. While the institutions that lend to large banks do not benefit from any official insurance from the government, they still know there is no chance of them not being repaid their money. This is because certain banks are considered too big or too important to fail. In the event that they went bust, the Government would be forced to step in to rescue them, which would include the payment of all of their outstanding liabilities (in effect this is what occurred with RBS). Because of this the ‘too big/important to fail’ institutions can borrow at cheaper rates than they would otherwise be able to, in a sense lending to them is effectively risk free – the government guarantees that it will repay if the bank is unable to.

This is outlined in detail in the Bank of England’s financial Stability Report:

[sws_blockquote_endquote align=”left” cite=”Bank of England, 2010, Financial Stability Report, p51″ quotestyle=”style02″ link=”http://www.bankofengland.co.uk/publications/Documents/fsr/2010/fsrfull1012.pdf”]The distress or failure of a systemically important financial institution (SIFI) is likely to entail large-scale economic costs. These costs engender expectations of government support and so allow SIFIs to benefit from an implicit funding subsidy from taxpayers … This subsidy encourages SIFIs to rely more heavily on debt finance … and to take on additional risk to maximise the value of the subsidy. [/sws_blockquote_endquote]

Without this subsidy the banks might not make any profit at all, and certainly wouldn’t be able to pay any bonuses:

[sws_blockquote_endquote align=”left” cite=”Robert Peston” quotestyle=”style02″ link=”http://www.bbc.co.uk/news/mobile/business-12022260″]it is quite difficult to see how they could ever generate a profit without this subsidy … in the absence of [the subsidy] the banks don’t really have any spare resources with which to pay bonuses [/sws_blockquote_endquote]

So, large banks require a public subsidy to be profitable and are too big/important to fail. This subsidy incentivises them to take risks they otherwise would not, increasing the likelihood of them failing. Of course, being too big to fail, when they do fail the government must step in to rescue them. Even the Governor of the Bank of England can’t see the sense in the system:

[sws_blockquote_endquote align=”left” cite=”Mervyn King, Banking: From Bagehot to Basel, and Back Again” quotestyle=”style02″ link=”http://www.bankofengland.co.uk/publications/Documents/speeches/2010/speech455.pdf”]it is hard to see why institutions whose failure cannot be contemplated should be in the private sector in the first place. [/sws_blockquote_endquote]

For further reading on this subject see Andrew Haldane’s 2010 paper, presentation and video (at 18:07).